How Mobile Phones Can Securely Authorize Payments Using Random ID Codes

A 2006 system that uses a mobile phone to receive and relay a unique, temporary ID code to a store terminal to verify and authorize a payment transaction.

Original patent title: “Method and apparatus of secure authentication and electronic payment through mobile communication tool”

A 2006 system that uses a mobile phone to receive and relay a unique, temporary ID code to a store terminal to verify and authorize a payment transaction. Granted to Individual in 2009 with 7 claims and 17 forward citations, and it is now in the public domain.

Coverage

What does this patent actually cover?

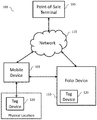

The system creates a secure loop between a user's phone, a store's transaction terminal, and a central account server. When a user initiates a purchase, the account server generates a one-time Random ID (RID) and sends it to the user's mobile phone. The user then transfers this RID to the store's terminal—via methods like Bluetooth, infrared, or by displaying it as a barcode for scanning. The store terminal sends the RID back to the account server, which confirms the match to authorize the payment.

The gap

What does this patent NOT cover?

- Does not cover payment systems that rely on static account numbers or credit card magnetic stripes without the RID verification loop.

- Does not cover biometric authentication (like fingerprint or facial recognition) as the primary verification mechanism.

- Does not cover direct peer-to-peer payments that bypass the central account server and transaction server architecture described in the claimsclaimsThe numbered statements at the end of a patent that legally define what the inventor owns.Read more →.

These exclusions are unique to PatentBrief — derived from the actual claim language, not patent-office boilerplate.

Key facts

What made this novel

The system uses the mobile device as a secure relay for a temporary token, effectively turning the phone into a dynamic 'key' that must be present at the physical point of sale to complete the transaction.

The Patent Drawing

Schematic visualization of the patent's claim structure. Hand-drawn diagrams in progress for each landmark patent.

Where you've seen this

Real-world examples

Mobile wallet barcode payment systems

Point-of-sale systems requiring a one-time code from a mobile app

Digital ticketing systems using dynamic QR codes

Why it matters

The bigger picture

This patent describes an early architecture for mobile-based payment verification, predating the widespread adoption of modern mobile wallets. It reflects a period when developers were solving the problem of how to securely bridge the gap between a user's mobile device and a physical point-of-sale terminal.

Filed

September 18, 2006

Granted

August 18, 2009

Market context

Who's building on this

Companies in this space

Major payment processors and mobile platform providers like Apple, Google, and Samsung have built upon the concept of tokenized mobile payments. While this specific patent is held by an individual, the industry has shifted toward standardized tokenization protocols like EMVCo to achieve similar security goals.

Market impact

This patent represents an early attempt to standardize mobile-to-terminal communication for payments. While it didn't spark a singular industry-wide lawsuit, it captures the technical transition from physical card-swiping to the era of mobile-mediated, token-based transactions that now dominate retail.

Claim 1 — Plain English

What this patent covers

The system creates a secure loop between a user's phone, a store's transaction terminal, and a central account server. When a user initiates a purchase, the account server generates a one-time Random ID (RID) and sends it to the user's mobile phone. The user then transfers this RID to the store's terminal—via methods like Bluetooth, infrared, or by displaying it as a barcode for scanning. The store terminal sends the RID back to the account server, which confirms the match to authorize the payment.

The clever bit

The system uses the mobile device as a secure relay for a temporary token, effectively turning the phone into a dynamic 'key' that must be present at the physical point of sale to complete the transaction.

What it does not cover

- Does not cover payment systems that rely on static account numbers or credit card magnetic stripes without the RID verification loop.

- Does not cover biometric authentication (like fingerprint or facial recognition) as the primary verification mechanism.

- Does not cover direct peer-to-peer payments that bypass the central account server and transaction server architecture described in the claims.

Patent timeline

Application submitted to the patent office

Application published, typically 18 months after filing

Patent officially issued

Patent enters public domain

PatentBrief Score

Impact Score

Early stage

Citation count

25/40

Moderately cited

Claim breadth

5/20

Moderate scope

Recency

5/20

Granted 10–20 years ago

Assignee scale

0/20

Independent or smaller assigneeassigneeThe entity that owns the patent — usually the inventor's employer or a company.Read more →

PatentBrief Impact Score — based on citation count, claim breadth, recency, and assignee scale. Not a legal assessment.

Heuristic Value Estimate

What this patent might be worth

$18K – $58K

Midpoint $36K · expired or expiring · industry ×1.6

Heuristic only — blends forward/backward citation counts, claim scope, time remaining, litigation history, and CPC-derived industry baseline. Real valuations need a professional appraisal.

Patent Claims

0 independent claims · 1 dependent

Claims are the legal boundaries of the patent. An independent claim stands alone. A dependent claim adds limitations to its parent, narrowing — but not broadening — the scope.

The original legal language

Original claims

7 claims as filed with the patent office.

Concepts involved

Citations

Patent lineage

Cite this patent

Zhu, X. (2009). How Mobile Phones Can Securely Authorize Payments Using Random ID Codes (U.S. Patent No. 7,577,616). U.S. Patent and Trademark Office. https://patentbrief.org/patent/us/7577616/method-and-apparatus-of-secure-authentication-and-electronic-payment-through-mobile-communication-tool

Auto-generated from the patent record. Double-check author order and the issue date against the official USPTO document before submitting.

Embed

Add this patent to your site

Drop this plain-English patent card into any blog post or article — free, no signup. It always links back to the full breakdown here.

<div data-patentlens-widget data-patent-number="US7577616"></div> <script src="https://patentbrief.org/embed.js" async></script>

Stay in the loop

Get a weekly digest of new patents.

One email per week. No spam. Unsubscribe anytime.

Keep exploring

Related patents you should know

US 4683195 · 1987

How to Make Billions of Copies of a DNA Segment

This patent describes the Polymerase Chain Reaction (PCR), a method to rapidly create many copies of a specific piece of DNA or RNA, enabling its detection and analysis.

Cetus Corp

US 8697359 · 2014

How to Edit Genes in Human Cells Using an Engineered CRISPR System

This patent describes an engineered CRISPR-Cas9 system for precisely cutting DNA in eukaryotic cells to change how genes work, opening the door for gene editing in complex organisms.

Massachusetts Institute of Technology

US 7657849 · 2010

How the iPhone's Slide-to-Unlock Gesture Works

Apple's 2010 patent describes unlocking a device by dragging a specific graphical image across the touchscreen along a predefined path, a gesture that became iconic with the original iPhone.

Apple Inc

US 4733665 · 1988

How Doctors Implant a Permanent Stent Using a Balloon

This patent describes the method for placing a permanent, expandable wire mesh tube inside a blood vessel or other body tube using a balloon-tipped catheter to widen it and keep it open.

Expandable Grafts Partnership

US 4965188 · 1990

How to Make Many Copies of a DNA Piece with Heat

This patent describes the Polymerase Chain Reaction (PCR) method, a technique to make millions of copies of a specific DNA segment using a heat-resistant enzyme and repeated temperature changes.

Cetus Corp

US 4235871 · 1980

How to Encapsulate Active Materials in Lipid Bubbles Efficiently

This patent describes a method for trapping biologically active substances inside tiny, multi-layered fat bubbles called liposomes, using a specific water-in-oil emulsion and gel-forming process to improve how much material gets captured.

Individual

Semantically similar

You might also find these interesting

US 10147076 · 2018

Central Bank Digital Currency for Phones and Watches

US 10198731 · 2019 · Square Inc

How Square Uses Your Phone's Location to Verify Credit Card Payments

US 10559047 · 2020 · NCR Corp

How Mobile Devices Use Tags to Close Restaurant Checks

US 5960411 · 1999 · Amazon com Inc

How Amazon's One-Click Ordering Works for Online Purchases

More to explore

More in Consumer Electronics

US 7657849 · 2010 · Apple Inc

How the iPhone's Slide-to-Unlock Gesture Works

US 7479949 · 2009 · Apple Inc

How Touchscreens Understand Your Finger Swipes and Scrolls

US 4528643 · 1985 · FPDC Inc

How Stores Make Custom Products On-Demand with Remote Approval

US 7469381 · 2008 · Apple Inc

How Touchscreens Show and Snap Back When You Scroll Past an Edge

New to patents?

Common Questions

Frequently Asked Questions

What does How Mobile Phones Can Securely Authorize Payments Using Random ID Codes cover?

A 2006 system that uses a mobile phone to receive and relay a unique, temporary ID code to a store terminal to verify and authorize a payment transaction.

Who owns patent US 7577616?

Individual owns this patent, granted in 2009.

When does this patent expire?

This patent is expected to expire on September 18, 2026, when the invention enters the public domain.

What is patent US 7577616 cited by?

This patent has been cited by 17 later patents that build on its ideas.

What problem does this patent solve?

This patent describes an early architecture for mobile-based payment verification, predating the widespread adoption of modern mobile wallets. It reflects a period when developers were solving the problem of how to securely bridge the gap between a user's mobile device and a physical point-of-sale terminal.

What does this patent NOT cover?

Does not cover payment systems that rely on static account numbers or credit card magnetic stripes without the RID verification loop.

Same assignee

More from Individual

Patent monitoring